The Relationship between Executive Compensation and Corporate Performance through Financial Risk Status of Listed Companies in The Stock Exchange of Thailand

Keywords:

Executive compensation, Corporate performance, Finance risk statusAbstract

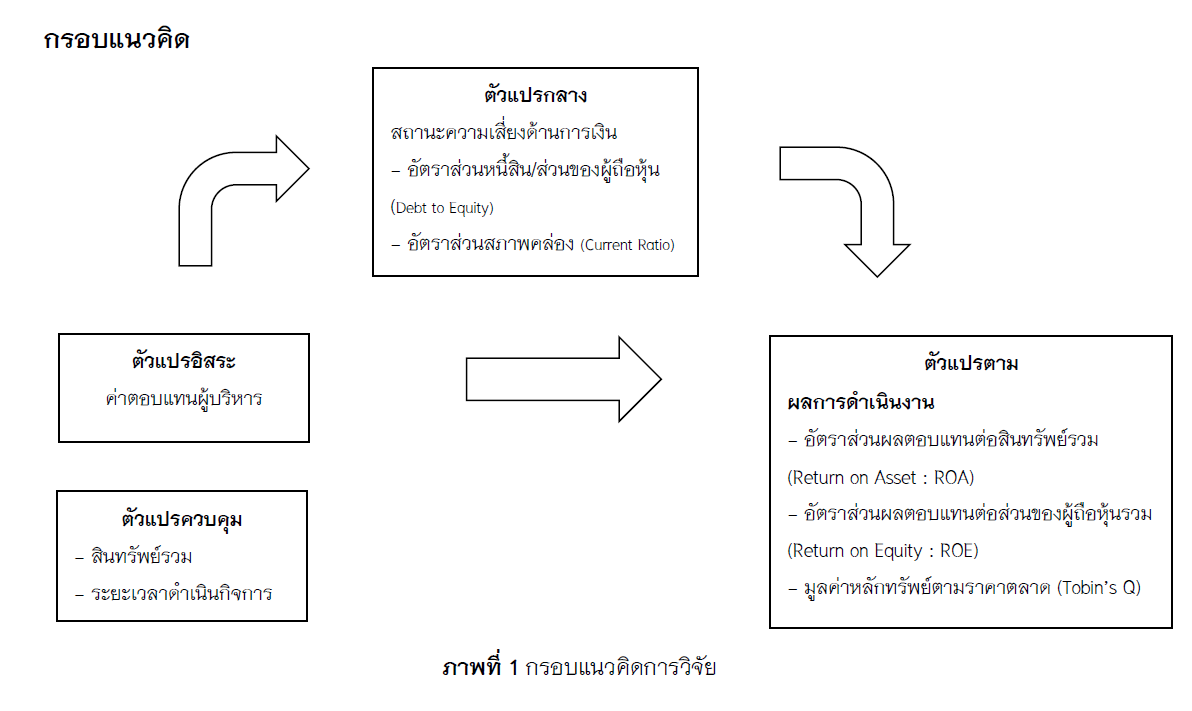

This research article aims to study the relationship between executive compensation and performance through financial risk status. The study was conducted using data from companies listed on the Stock Exchange of Thailand in 2021-2023, totaling 1,531 data, and using descriptive statistics and multiple regression statistics to analyze the data. The results of the study found that executive compensation had a positive relationshipwith performance at a statistical significance level of 0.01, indicating that setting appropriate compensation motivates executives to manage their work more efficiently. Meanwhile, financial risk status, measured by the debt-to-equity ratio, had a negative relationship with the return on total assets (ROA) ratio and the return on total equity (ROE) ratio at a statistical significance level of 0.01, reflecting that organizations with high debt burden tend to have lower profit performance. However, there was a statistically insignificant positive relationship with the market value (Tobin’s Q), which may indicate that the market’s perception has not yet clearly responded to capital structure risk. At the same time, the liquidity ratio did not significantly influence performance in any dimension, indicating that the ability to pay short-term debts alone may not be an important variable affecting the overall performance of the organization. Especially when compared to the debt burden in the capital structure that has a clearer effect on the ability to generate returns. In addition, it was found that executive compensation is not related to the financial risk status. This indicates that the financial risk status cannot be a variable that transmits between executive compensation and performance. This study can provide insights into the role of executive compensation in driving the organization's performance, which can help companies determine appropriate compensation that is consistent with performance. In addition, the results of the study can be a guideline for developing risk management strategies, especially in terms of finance, which, although it does not affect performance in all aspects, can play a role in terms of image, transparency, and building confidence from investors.

References

กมลพร วรรณชาติ, บุษบรรณณ์ เหลี่ยวรุ่งเรือง และ ชิดชนก มากเชื้อ. (2559). ความสัมพันธ์ระหว่างคุณลักษณะขององค์กร การเปิดเผยข้อมูลการบริหารความเสี่ยงตามกรอบแนวคิดของ COSO และผลการดำเนินงานของบริษัทใน SET 100. สงขลา: คณะบริหารธุรกิจ มหาวิทยาลัยเทคโนโลยีราชมงคลศรีวิชัย.

ชุดาพร สอนภักดี, ธาวินี สุขมี, พิมพ์ชนก อิทธิพัทธ์วรกุล, สรัญญา เอี่ยมอำนวย, ชมพูนุช อินทร์ขาว และ อารียา ผิวเผือด. (2567). ความสัมพันธ์ระหว่างคะแนนการกำกับดูแลกิจการ ค่าตอบแทนคณะกรรมการกับผลการดำเนินงานของบริษัทที่จดทะเบียนในตลาดหลักทรัพย์เอ็ม เอ ไอ (MAI). วารสารวิทยาการจัดการ มหาวิทยาลัยราชภัฏอุดรธานี, 6(5), 11-23.

ธัญญ์นรี แซ่โง้ว. (2557) ความสัมพันธ์ระหว่างค่าตอบแทนคณะกรรมการบริษัทและสัดส่วนผู้บริหารหญิงกับผลตอบแทนของผู้ ถือหุ้นของบริษัทที่จดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย กลุ่ม SET100. (การค้นคว้าแบบอิสระหลักสูตรบริหารธุรกิจมหาบัณฑิต). กรุงเทพฯ: มหาวิทยาลัยกรุงเทพ.

ธีรพรรณ อึ้งภากรณ์, ไตรรงค์ สวัสดิกุล, สุชิตา มานะจิตต์ และ วิชนี เอี่ยมชุ่ม. (2560). ผลกระทบของคุณภาพการเปิดเผยข้อมูลความเสี่ยงที่มีต่อผลการดำเนินงาน: กรณีศึกษาบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย. วารสารการบัญชีและการจัดการ มหาวิทยาลัยมหาสารคาม, 11(2), 118–126.

นงลักษณ์ ผุดเผือก และ สุรีย์ โบษกรนัฏ. (2566). องค์ประกอบคณะกรรมการบริหารความเสี่ยงและคณะกรรมการตรวจสอบที่มีอิทธิพลต่อผลการดำเนินงานและผลตอบแทนหลักทรัพย์ของบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย. วารสารศิลปะการจัดการ, 7(3), 1108-1135.

นิตติกร สุวรรณศิลป์, ธนัชพร แก้วทอง, นวลอนงค์ แก้วสายทอง, นันทวดี ลดาพรหมทอง, สุภาพร เกาะเต้น และ มัทนชัย สุทธิพันธุ์. (2561). การศึกษาเปรียบเทียบการเปิดเผยข้อมูลความเสี่ยงของบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย (SET) กับตลาดหลักทรัพย์ เอ็ม เอ ไอ (MAI) และความสัมพันธ์ระหว่างการเปิดเผยข้อมูลความเสี่ยงกับต้นทุนหนี้สิน. วารสารหาดใหญ่วิชาการ, 16(2), 153-170.

ปริณดา แสงวณิชวัฒนา. (2563). ผลกระทบของค่าตอบแทนผู้บริหารและคณะกรรมการบริษัทต่อผลการดำเนินงาน ของกิจการผ่านการบริหารความเสี่ยง. (การค้นคว้าแบบอิสระหลักสูตรวิทยาศาสตรมหาบัณฑิต การบัญชีและการบริหารการเงิน). กรุงเทพฯ: มหาวิทยาลัยธรรมศาสตร์.

ปรียานุช อยู่สังข์. (2558). ความสัมพันธ์ระหว่างผลการดำเนินงานกับคุณภาพการเปิดเผยข้อมูลความเสี่ยงของบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย. การประชุมวิชาการระดับชาติ ราชภัฏเพชรบุรีวิจัยเพื่อแผ่นดินไทยที่ยั่งยืนครั้งที่ 5. เพชรบุรี: มหาวิทยาลัยราชภัฏเพชรบุรี

ปวันรัตน์ โรจน์รักษกุล. (2562). การศึกษาความสัมพันธ์ระหว่างการเปิดเผยปัจจัยความเสี่ยงในรายงานประจำปีกับผลการดำเนินงานของบริษัทที่จดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย. (การค้นคว้าแบบอิสระหลักสูตรบัญชีมหาบัณฑิต). กรุงเทพฯ: มหาวิทยาลัยธรรมศาสตร์.

ปิยะณัฐ กาญจนารัตน์ (2564). ความสัมพันธ์ระหว่างอัตราส่วนทางการเงิน กระแสเงินสด และมูลค่ากิจการของบริษัทที่จดทะเบียนในตลาดหลักทรัพย์: กรณีศึกษาประเทศในกลุ่มโครงการพัฒนาเขตเศรษฐกิจสามฝ่ายอินโดนีเซีย มาเลเซีย และไทย. (วิทยานิพนธ์หลักสูตรบัญชีมหาบัณฑิต). สงขลา: มหาวิทยาลัยสงขลานครินทร์.

พจนารถ ฤทธิเดช, ปาริชาติ บูรพาศิริวัฒน์ และ มัทนชัย สุทธิพันธุ์. (2564). อิทธิพลของผลตอบแทนผู้บริหารต่อผลการดำเนินงานทางการเงินของบริษัทที่จดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย. วารสารการบัญชีและการจัดการ มหาวิทยาลัยมหาสารคาม, 13(2), 60-74.

พรพิพัฒน์ จูฑา. (2548) ความสัมพันธ์ระหว่างคุณภาพของการเปิดเผยความเสี่ยงกับผลการดำเนินงานทางการเงินของบริษัทที่จดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย. (วิทยานิพนธ์บัญชีมหาบัณฑิต). กรุงเทพฯ: จุฬาลงกรณ์มหาวิทยาลัย.

พรรณวดี แซ่ฉั่ว และ สมใจ บุญหมื่นไวย. (2562). ความสัมพันธ์ระหว่างธุรกิจครอบครัว ค่าตอบแทนผู้บริหาร และผลการดำเนินงานของบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย. KKBS Journal of Business Administration and Accountancy, 3(2), 75-96.

พิธาน แสนภักดี และ นฤพล อ่อนวิมล. (2564). คุณลักษณะและค่าตอบแทนของผู้บริหารที่มีอิทธิพลต่อผลการดำเนินงานของบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย. วารสารมนุษยศาสตร์และสังคมศาสตร์ มหาวิทยาลัยราชพฤกษ์, ฉบับพิเศษ ฉลองครบรอบ 15 ปี มหาวิทยาลัยราชพฤกษ์, 385-397.

ภูษณิศา ส่งเจริญ. (2564). ความสัมพันธ์ระหว่างอัตราส่วนทางการเงินและอัตราผลตอบแทนจากสินทรัพย์ของบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย. วารสารรัชต์ภาคย์, 15(38), 30-41.

วรรณภา ธรรมรักษา, เนตรนภา รักษายศ และ สารภี ชนะทัพ. (2567). ความสัมพันธ์ระหว่างคุณลักษณะของบริษัทกับการเปิดเผยข้อมูลการบริหารความเสี่ยงของบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย กลุ่ม SET50. วารสารบัญชีปริทัศน์ มหาวิทยาลัยราชภัฎเชียงราย, 9(2), 115-136.

สมบูรณ์ สาระพัด. (2565). ผลกระทบการเปิดเผยข้อมูลความยั่งยืนที่มีต่อผลการดำเนินงานของบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย. วารสารวิทยาการจัดการ มหาวิทยาลัยเกษตรศาสตร์, 1(2), 56-81.

สำนักงานคณะกรรมการกำกับหลักทรัพย์และตลาดหลักทรัพย์. (2558). ประกาศคณะกรรมการกำกับตลาดทุน ที่ ทจ. 17/2558: เรื่อง หลักเกณฑ์ เงื่อนไข และวิธีการรายงานการเปิดเผยข้อมูลเกี่ยวกับฐานะการเงินและผลการดำเนินงานของบริษัทต่างประเทศที่ออกและเสนอขายหุ้น.

อรุณี ยศบุตร. (2564). ลักษณะการจ่ายค่าตอบแทนกรรมการกับผลการดำเนินงานของบริษัท:หลักฐานเชิงประจักษ์จากบริษัทจดทะเบียนในตลาดหลักทรัพย์เอ็ม เอ ไอ ประเทศไทย. วารสารมนุษยศาสตร์และสังคมศาสตร์ มหาวิทยาลัยพะเยา, 9(1), 233-255.

Baroma, B. S. (2020). The effect of voluntary disclosure and transparency on directors´ remuneration control. Alexandria Journal of Accounting Research, 4(3), 1-36.

Bao, H. D. (2023). Financial aspects and financial risk disclosure: evidence from Vietnam. Economics, Finance and Management Review, (3), 39-48.

Freeman, R. E., Harrison, J. S., Wicks, A. C., Parmar, B. L., & de Colle, S. (2010). Stakeholder theory: The state of the art. Cambridge University Press.

Heinle, M. S., & Smith, K. C. (2017). A theory of risk disclosure. Review of Accounting Studies, 22(4), 1459–1491.

Ibrahim, A. E. A., & Aboud, A. (2024). Corporate risk disclosure and firm value: UK evidence. International Journal of Finance & Economics, 29(4), 4225-4246.

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360.

Oyerogba, E. O. (2014). Risk disclosure in the published financial statements and firm performance: Evidence from The Nigeria Listed Companies. Journal of Economics and Sustainable Development, 5(8), 86-95.

Qizam, I. (2021). The impact of disclosure quality on firm performance: Empirical evidence from Indonesia. The Journal of Asian Finance, Economics and Business, 8(4), 751-762.

Salehi, M., Jamalikazemini, B., & Farhangdoust, S. (2018). Board compensation and disclosure quality: Corporate governance interference. Journal of Asian Finance, Economics and Business, 8(4), 751-762.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Phayao University

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

ผู้นิพนธ์ต้องรับผิดชอบข้อความในบทนิพนธ์ของตน มหาวิทยาลัยพะเยาไม่จำเป็นต้องเห็นด้วยกับบทความที่ตีพิมพ์เสมอไป ผู้สนใจสามารถคัดลอก และนำไปใช้ได้ แต่จะต้องขออนุมัติเจ้าของ และได้รับการอนุมัติเป็นลายลักษณ์อักษรก่อน พร้อมกับมีการอ้างอิงและกล่าวคำขอบคุณให้ถูกต้องด้วย

The authors are themselves responsible for their contents. Signed articles may not always reflect the opinion of University of Phayao. The articles can be reproduced and reprinted, provided that permission is given by the authors and acknowledgement must be given.