The Effects of Risk Assessment Process on Operational Efficiency of Accounting Firms in Udon Thani Province

Keywords:

Risk assessment process, Operational efficiency, Accounting firmsAbstract

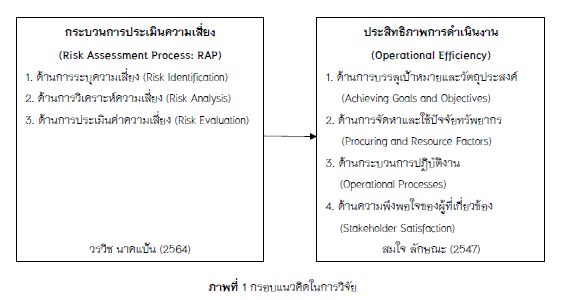

This research aimed to: (1) study the relationship between the risk assessment process and the operational efficiency of accounting firms in Udon Thani Province, and (2) examine the effects of the risk assessment process on the operational efficiency of accounting firms in Udon Thani Province. A questionnaire was used to collect data from 64 accounting firms. Statistical methods employed for data analysis included multiple correlation analysis and multiple regression analysis.

The results of this research found that 1) risk assessment process, in risk identification, risk analysis and risk evaluation, There was a statistically significant positive correlation with both overall and individual aspects of operational efficiency at the 0.05 level. 2) Overall risk assessment process, in risk identification, risk analysis and risk evaluation, has a statistically significant positive impact on both overall and individual aspects of operational efficiency at the 0.05 level. The findings of this study indicate that the risk assessment process is a vital mechanism that plays a significant role in enhancing the quality and efficiency of operational performance. Therefore, accounting firms should prioritize the implementation of a systematic and continuous risk assessment process in order to strengthen operational stability, improve competitive advantage, and lead the organization toward long-term sustainability.

References

กรมพัฒนาธุรกิจการค้า. (2564). ประกาศกรมพัฒนาธุรกิจการค้า เรื่อง หลักเกณฑ์และเงื่อนไขในการรับรองคุณภาพ สำนักงานบัญชี พ.ศ. 2564. สืบค้น 20 กุมภาพันธ์ 2568, จาก https://www.dbd.go.th/data-storage/attachment/1d74254875aaf47a10ed33e4a.pdf.

กรมพัฒนาธุรกิจการค้า. (2568). รายชื่อสำนักงานบริการรับทำบัญชีจังหวัดอุดรธานี. สืบค้น 20 กุมภาพันธ์ 2568, จาก https://www.dbd.go.th/storage/manual/6a652e36-8f6a-49cb-a54e-0c733551e82b.pdf.

เง็กไน้ แซ่ลี้. (2559). การบริหารความเสี่ยงที่ส่งผลต่อการบริหารงานพัสดุของสถานศึกษาสังกัดสำนักงานคณะกรรมการการอาชีวศึกษา จังหวัดสุพรรณบุรี. วารสารศิลปากรศึกษาศาตร์วิจัย, 9(1), 329–343.

จันทนา สาขากร, นิพันธ์ เห็นโชคชัยชนะ และ ศิลปพร ศรีจั่นเพชร. (2557). การควบคุมภายในและการตรวจสอบภายใน. กรุงเทพฯ: ห้างหุ้นส่วนจำกัด ทีพีเอ็น เพรส.

นิรัช สุดสังข์. (2559). ระเบียบวิธีวิจัยทางการออกแบบ (พิมพ์ครั้งที่ 1). กรุงเทพฯ: โอเดียนสโตร์.

พัฒนา ร่มเย็น. (2562). ผลกระทบของการบริหารความเสี่ยงในการปฏิบัติงานทางการเงินที่มีผลต่อความสำเร็จในการดำเนินงานขององค์กรปกครองส่วนท้องถิ่นในเขตภาคเหนือตอนบน. วารสารบัณฑิตศึกษา มหาวิทยาลัยราชภัฏเชียงราย, 12(3), 47–63.

วรวิช นาคแป้น. (2564). การประเมินความเสี่ยง (Risk Assessment) และ การจัดการความเสี่ยง (Risk Treatment). สืบค้น 10 มีนาคม 2568, จาก https://www.ohswa.or.th/17880442/ซีรีส์ความเสี่ยงเลี่ยง-ไม่-ได้-ep6.

สภาวิชาชีพบัญชี. (2568). ประเมินความเสี่ยงในสำนักงานสอบบัญชีเริ่มอย่างไรดี. สืบค้น 24 มกราคม 2568, จาก https://acpro-std.tfac.or.th/test_std/uploads/files/มาตรฐานสอบบัญชี/ประเมินความเสี่ยงในสำนักงานสอบบัญชีเริ่มอย่างไรดี_post.pdf.

สมใจ ลักษณะ. (2547). การพัฒนาประสิทธิภาพในการทำงาน. กรุงเทพฯ: สถาบันราชภัฏสวนสุนันทา.

สมยศ อวเกียรติ และ สิทธิพร ประวัติรุ่งเรือง. (2560). การบริหารความเสี่ยงที่มีความสัมพันธ์กับผลการดำเนินงานของธุรกิจขนาดกลางและขนาดย่อมในจังหวัดปทุมธานี. วารสารวิชาการมหาวิทยาลัยฟาร์อิสเทอร์น, 11(4), 48–62.

Aaker, D. A., Kumar,V. & Day, G.S. (2010). Marketing Research (7th ed.). New York: JohnWiley & Sons.

Black, k. (2006). Business statistics for contemporary decision marking (4th ed.). New York: John Wiley & Sons.

Nunnally, J. C. (1978). Psychometric Theory. New York: McGraw-Hill.

Nunnally, J. C., & Bernstein, I. H. (1994). Psychometric theory (3rd ed.). New York: McGraw- Hill.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Phayao University

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

ผู้นิพนธ์ต้องรับผิดชอบข้อความในบทนิพนธ์ของตน มหาวิทยาลัยพะเยาไม่จำเป็นต้องเห็นด้วยกับบทความที่ตีพิมพ์เสมอไป ผู้สนใจสามารถคัดลอก และนำไปใช้ได้ แต่จะต้องขออนุมัติเจ้าของ และได้รับการอนุมัติเป็นลายลักษณ์อักษรก่อน พร้อมกับมีการอ้างอิงและกล่าวคำขอบคุณให้ถูกต้องด้วย

The authors are themselves responsible for their contents. Signed articles may not always reflect the opinion of University of Phayao. The articles can be reproduced and reprinted, provided that permission is given by the authors and acknowledgement must be given.