ความสัมพันธ์ระหว่างคะแนนการกำกับดูแลกิจการกับราคาหลักทรัพย์: หลักฐานเชิงประจักษ์บริษัทที่จดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย

คำสำคัญ:

การกำกับดูแลกิจการ, ขนาดของคณะกรรมการบริษัท, ความเป็นอิสระของคณะกรรมการ, ราคาหลักทรัพย์บทคัดย่อ

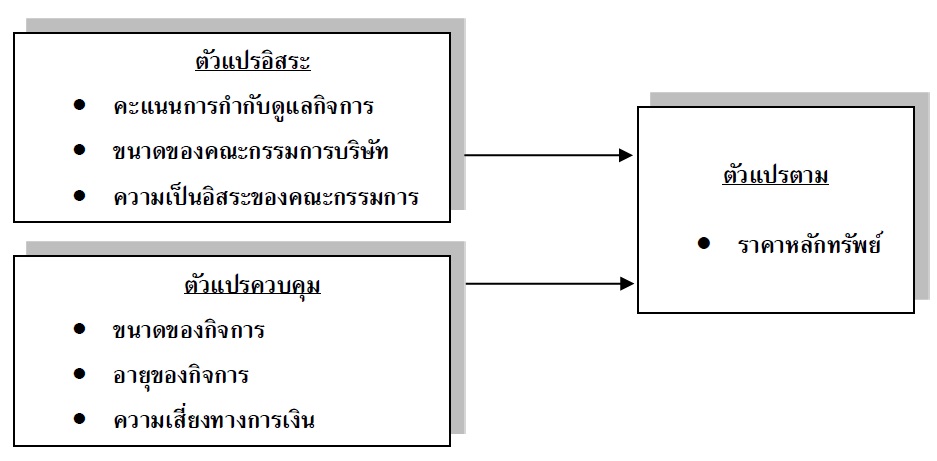

งานวิจัยนี้มีวัตถุประสงค์เพื่อศึกษาความสัมพันธ์ระหว่างการกำกับดูแลกิจการ ขนาดของคณะกรรมการบริษัท และความเป็นอิสระของคณะกรรมการกับราคาหลักทรัพย์ของบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย โดยเก็บรวบรวมข้อมูลอันดับคะแนนการกำกับดูแลกิจการ ขนาดของความเป็นอิสระของคณะกรรมการบริษัท และราคาหลักทรัพย์ของบริษัทจดทะเบียนในตลาดหลักทรัพย์ ปี 2561 - ปี 2562 และ ปี 2563 จำนวน 494 บริษัท 521 บริษัท และ 544 บริษัท ตามลำดับ ตัวแบบความสัมพันธ์เชิงเส้นตรงที่ใช้มีขนาดของกิจการ อายุของกิจการ และความเสี่ยงทางการเงิน เป็นตัวแปรควบคุม ใช้วิธีการวิเคราะห์ความถดถอยเชิงพหุในการตรวจสอบความสัมพันธ์ระหว่างราคาหลักทรัพย์ และคะแนนการกำกับดูแลกิจการ กับขนาดและความเป็นอิสระของคณะกรรมการบริษัท ผลการวิจัยชี้ให้เห็นว่าขนาดและความเป็นอิสระของคณะกรรมการ มีความสัมพันธ์เชิงบวกกับราคาหลักทรัพย์อย่างมีนัยสำคัญทางสถิติ ที่ช่วงความเชื่อมั่น 95% แต่ไม่พบความสัมพันธ์ระหว่างคะแนนการกำกับดูแลกิจการกับราคาหลักทรัพย์ ในขณะที่ตัวแปรควบคุม คือ ขนาดของกิจการมีความสัมพันธ์เชิงบวกและความเสี่ยงทางการเงินมีความสัมพันธ์เชิงลบกับราคาหลักทรัพย์อย่างมีนัยสำคัญทางสถิติ ที่ช่วงความเชื่อมั่น 95% โดยไม่พบความสัมพันธ์ระหว่างอายุของกิจการกับราคาหลักทรัพย์ ข้อมูลขนาดและความเป็นอิสระของคณะกรรมการบริษัทจึงเป็นข้อมูลที่นักลงทุนให้ความสนใจ

เอกสารอ้างอิง

ตลาดหลักทรัพย์แห่งประเทศไทย. หลักการกำกับดูแลกิจการที่ดีสำหรับบริษัทจดทะเบียน 2560 [อินเตอร์เน็ต]. 2560 [เข้าถึงเมื่อวันที่ 24 มีนาคม 2564]. เข้าถึงได้จาก http://www.sec. or.th/cgthailand/th/Documents/Regulation/CGCode.pdf/.

สำนักงานคณะกรรมการกำกับหลักทรัพย์และตลาดหลักทรัพย์. การกำกับดูแลกิจการที่ดีและการพัฒนากิจการเพื่อความยั่งยืน [อินเตอร์เน็ต]. 2560 [เข้าถึงเมื่อวันที่ 12 เมษายน 2564]. เข้าถึงได้จากhttp://www.sec.or.th/cgthailand/th/pages/overview/cgandsustainablebusinessdevelopment.aspx/.

Klapper LF, Love I. Corporate governance, investor protection, and performance in emerging markets. Journal of Corporate Finance 2004;10(5):703-28.

Berthelot S, Morris T, Morrill C. Corporate governance rating and financial performance: A Canadian study. Corporate Governance 2010; 10(5):635-46.

ทิพย์ธัญญา หริณานนท์. อิทธิพลของการกำกับดูแลกิจการที่มีต่อการจัดการกำไรและมูลค่าเพิ่มเชิงเศรษฐศาสตร์: กรณีศึกษาบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย กลุ่ม SET 100 [วิทยานิพนธ์ปริญญาบัญชีมหาบัณฑิต]. สงขลา: มหาวิทยาลัยสงขลานครินทร์; 2560.

La Porta F L, Shleifer A, Vishny A. Legal determinants of external finance. Journal of Finance 1997;2(7):1131-50.

Jensen MC, Meckling WH. Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics 1976;2:305-60.

Bhagat S, Bolton B. Corporate governance and firm performance. Journal of Corporate Finance 2008;14(3):257-73.

Gompers PA, Ishiii JL, Metrick A. Corporate governance and equity prices. Quarterly Journal of Economics 2003;118:107-55.

Brown LD, Caylor ML. Corporate governance and firm valuation. Journal of Accounting and public Policy 2006;25(4):409-34.

Firmansyah A, Triastie GA. The role of corporate governance in emerging market: Tax avoidance, corporate social responsibility disclosures, risk disclosures, and investment efficiency. Journal of Governance and Regulation 2020;9(3):8-26.

Gulzar MA, Wang Z. Corporate governance characteristics and earnings management: Empirical evidence from Chines Listed Firms, International Journal of Accounting and Financial Reporting 2011;1(1):133-51.

Tarus TK, Tenai J, Komen J. Effect of audit committee size on risk management: Evidence from selected listed firms in Kenya. International Journal of Research and innovation in Social Science 2019;3(5):437-43.

Brown LD, Caylor ML. Corporate governance and firm valuation. Journal of Accounting and Public Policy 2006;25(4):409-34.

Utami W, Pernamasari R. Study on ASEAN listed companies: Corporate governance and firm performance. International Journal of Business, Economics and Law 2019;19(5): 181-8.

Dzingai I, Fakoya BM. Effect of corporate governance structure on the financial performance of Johannesburg Stock Exchange (JSE) listed mining firms. Sustainability 2017;9(876):1-15.

Whelan C. The value relevance of corporate governance: Australian evidence. Corporate Ownership and Control 2007;4(4):292-8.

Yasa GW, Astika IP, Widiariani NA. The influence of accounting conservatism, los, and good corporate governance on the earning quality. Journal IImiah Akuntansi dan Bisnis, 2019;14(1):86-94.

Enache L, Garcia-Meca E. Board composition and accounting conservatism: The role of business experts, support specialist and community influential. Australian Accounting Review 2019;29(88):252-65.

Rahman RA, Ali FHM. Board, audit committee, culture and earnings management: Malaysian evidence. Managerial Auditing Journal 2006;27:783-804.

Oludele OI, Oloko MA, Tobiah O. The relationship between board independence and financial performance of listed manufacturing companies in Nigeria. European Journal of Business, Economics and Accountancy 2016; 4(9):45-56.

Berthelot S, Morris T, Morrill C. Corporate Governance Rating and Financial Performance: A Canadian study. Corporate Governance 2010;10(5):635-46.

Francis J, Schipper K, Vincent L. The relative and incremental explanatory power of earnings and alternative performance measures for return. Contemporary Accounting Research 2003;20(1):121-64.

Yoon S, Miller GA, Jiraporn P. Earning management vehicles for Korean firms. Journal of International Financial Management and Accounting 2006;17(2):85-109.

Rountree B, Weston J, Allayannis G. “Do investors value smooth performance?” Journal of Financial Economic 2008;90:237-57.

DeAngelo H, DeAngelo L, Stulz RM. Dividend policy and the earned/contributed capital mix: A test of the life-cycle theory. Journal of Financial Economics 2006; 81(2):227-54.

Kim HJ, Yoon SS. The impact of corporate government on earnings management in Korea. Malaysian Accounting Review 2008;7(1): 43-59.

Zhang Y, Lu G. Study on differences in correlation between the accounting data and stock price of China and Thailand base on Ohlson model. Advance in Economics, Business and Management Research 2018; 58:329-34.

Thai Institute of Directors Association. IOD Corporate Governance Reports of Thai Listed Companies. Bangkok: The Institute; 2018.

Thai Institute of Directors Association. IOD Corporate Governance Reports of Thai Listed Companies. Bangkok: The Institute; 2019.

Thai Institute of Directors Association. IOD Corporate Governance Reports of Thai Listed Companies. Bangkok: The Institute; 2020.

Hodgson A, Lhaopadchan S, Buakes S. How Informative is the Thai Corporate Governance Index? A Financial Approach. International Journal of Accounting and Information Management 2011;19(1):53-79.

ชูศรี วงศ์รัตนะ. เทคนิคการใช้สถิติเพื่อการวิจัย. กรุงเทพมหานคร: จุฬาลงกรณ์มหาวิทยาลัย; 2562.

ณัฐนันท์ บัวสาย. ความมีคุณค่าของข้อมูลของตัววัดผลการดำเนินงานทางการบัญชี: กรณีศึกษาตลาดหลักทรัพย์แห่งประเทศไทย [การค้นคว้าอิสระปริญญาบัญชีมหาบัณฑิต]. กรุงเพมหานคร: มหาวิทยาลัยธรรมศาสตร์; 2558.

Gupta PP, Kennedy BD, Weaver CS. Corporate governance and firm value: Evidence from Canadian capital markets. Corporate Ownership and Control 2009;6(3):293-307.

อรพรรณ เลิศรุจิวณิช. ความสัมพันธ์ระหว่างการกำกับดูแลกิจการที่ดี การป้องกันการมีส่วนเกี่ยวข้องกับคอร์รัปชั่นและมูลค่ากิจการของบริษัทจดทะเบียนในตลาดหลักทรัพย์ แห่งประเทศไทย [การค้นคว้าอิสระปริญญาบัญชีมหาบัณฑิต]. กรุงเทพมหานคร: มหาวิทยาลัยธรรมศาสตร์; 2559.

วิภาดา ภาโนมัย และ นงค์นิตย์ จันทร์จรัส. โครงสร้างคณะกรรมการบริหารกับผลการดำเนินงานของบริษัทจดทะเบียนกลุ่มธุรกิจอาหารและเครื่องดื่มประเทศไทย. วารสารวิทยาการจัดการสมัยใหม่ 2559;5(2):44-55.

El-habashy HA. The effect of corporate governance attributes on accounting conservatism in Egypt. Academy of Accounting and Financial Studies Journal 2019;23(3):1-18.

Affes H, Sardouk H. Accounting conservatism and corporate performance: The moderating effect of the board of directors. Journal of Business and Financial Affairs 2016;5(2):1-8.

Ahmed K, Henry D. Accounting conservatism and voluntary corporate governance mechanisms by Australian firms. Accounting and Finance 2012;(52):631-62.

ดาวน์โหลด

เผยแพร่แล้ว

ฉบับ

ประเภทบทความ

สัญญาอนุญาต

บทความทุกบทความที่ตีพิมพ์ในวารสารการพัฒนางานประจำสู่งานวิจัย (JPR2R) ถือว่าเป็นลิขสิทธิ์ของวารสารการพัฒนางานประจำสู่งานวิจัย คณะสิ่งแวดล้อมและทรัพยากรศาสตร์ มหาวิทยาลัยมหิดล